With the recession looming, our Government will definitely be looking at bringing CGT (Capital Gains Tax) in one form or another. Not quite up to date with the CGT situation in NZ? Ok, here’s a brief summary:

Capital Gains Tax is tax paid on any capital gains you make.

What are capital gains?

Simply put – capital gains are any gains you make from selling property, shares or any other form of asset which is not part of your regular business/wage income.

A capital gains tax is basically tax on capital gains that you make.

Essentially, a capital gains tax is a way for the government to tax an additional income source which usually wouldn’t be taxed.

In NZ, there are many arguments for and against the implementation of CGT, which has turned it into a hot political issue, which has led to its implementation being blocked, delayed and altogether relegated to the ‘too sensitive to touch’ pile of political hubbub. However, the COVID-19 crisis has spurred the government into action with the $12.1 billion financial aid package which almost certainly will have to be paid for with new and innovative means of taxing kiwis.

And trust me when I say that CGT will definitely be on that list of taxes they will be looking at.

So the implementation of some form of CGT is inevitable. But there are still a lot of arguments against it. Before I propose what I feel is a fair and balanced way of implementing it, let’s look at some of the common arguments posed against CGT:

But NZ ALREADY HAS CGT!

Uh, not exactly – what NZ has is the bright-line test. When you purchase a property – if you sell it within 5 years of purchasing it, you will have to add in any gains made on the sales (Sales price – purchase price) as taxable income to your income tax calculation.

More often than not, this will cause your income tax for the year to spike and whatever gains you made from the property sales will likely be taxed at the highest tax bracket of 33%.

But if you sell the property after 5 years you don’t pay any taxes on the gains made from selling.

Which is weird and arbitrary because no one in their right mind would sell their property within 5 years and risk paying a 33% tax on their gains but suddenly at 5 years and 1 day they can sell it off, tax-free. Not a very practical or elegant system in my opinion.

But CGT will hurt all the Mum and Dad investors!

Generally speaking – this is the most common line of argument against CGT that you will hear. The fear is that, with CGT, all the investments that Mum and Dad have put into shares and property will become taxable the minute they decide to cash out their investments and sell them. To be fair, it is a reasonable fear.

Can you imagine having built up an investment portfolio of shares and property which you have carefully managed over 20 years and finally when you are ready to cash out those assets – you have to pay a butt-ton of tax on them.

Ouch.

Not pleasant at all for everyone looking to retire, hence the strong opposition to CGT coming from boomers.

To all my fellow millennials out there – you may say ‘Ok, Boomer’ now but just you wait until you’re ready to retire and the Government throws a 33% CGT at your retirement portfolio and let’s see how you feel when snarky zoomers come up to you and say ‘Ok, Millenial’ and roll their eyes at you.

So yeah, CGT needs to be done in a way that doesn’t penalise people saving up for retirement.

The common arguments against CGT have been outlined and some of the points they make are valid. However, CGT remains an effective way for the government to bring in additional tax revenue which will hopefully be reinvested into economic infrastructure which can help us pay down the debt incurred via the financial stimulus package.

So how do we come up with a fair and balanced CGT?

My proposition is to not reinvent the wheel but to simply look to other countries for inspiration.

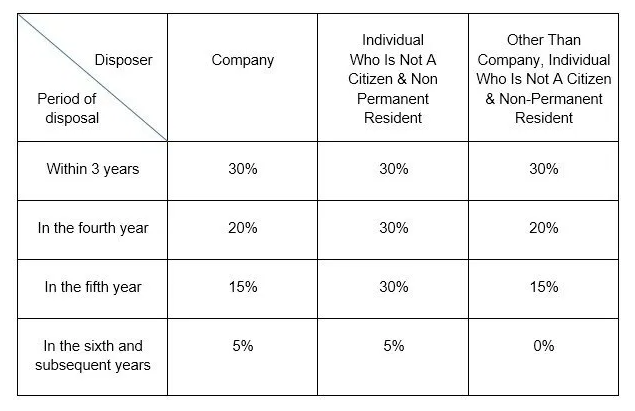

Back in my home country of Malaysia, we’ve had a form of CGT on property sales called Real Property Gains Tax (RPGT) which is taxed separately to your income tax and is based off the gains made from the sales of the property.

The RPGT in Malaysia is quite simple. Take the disposal (selling) price, minus the acquisition (buying) price and minus any other incidental costs (Lawyer fees etc) and boom – you have the taxable RPGT profit.

RPGT in Malaysia is calculated based on a very simple scale rate which is determined by how many years you have held the property for:

Basically, if you are a regular Malaysian Citizen (not a company), if you dispose of property within 3 years, you pay 30% RPGT. In 4 years, you pay 20% RPGT. In 5 years you pay 15% RPGT and in the 6th year and beyond – you pay 0% tax.

Also – Malaysia taxes their non-residents really high, but I won’t comment on that.

So how can we adapt such a model to NZ?

Simple – CGT could be applied on a similar scale rate basis that decreases the longer you hold the asset for, with the maximum time period resulting in 0% tax. This can be applied to both properties and shares. With tax applicable on the gain made from the sale of the asset (disposal price – acquisition price).

We shouldn’t follow the Malaysian system word for word, I think there is some room to adapt it for usage within a local kiwi context. My suggestion would be to apply a scale rate as follows for applying CGT (note that this is purely an academic suggestion and should be thoroughly debated):

| Period of Disposal | Tax rate to individual |

| Within 2 years | 33% |

| Within 5 years | 17.5% |

| Within 7 years | 10.5% |

| Within 10 years | 5% |

| In the 10th and subsequent years | 0% |

CGT should be calculated separately from income tax so that it doesn’t mess up your standing on the income tax scale rate. As an added bonus – this is yet another service your accountant can charge you for which is separate to your income tax (yay for us accountants!).

So why the scale rate?

Simply because – it captures any income made by individuals who invest in shares and properties for speculative reasons. Any individuals looking to make a short term gain will have to pay the taxes associated with it. That way tax is captured on their income and hopefully it will discourage speculative behaviour in the property market and to a lesser extent, the local share market. At the same time, it does not penalise individuals who are looking at building up their retirement portfolio and saving up for the long term

I will point out that the scale rates I’ve suggested are by no means perfect and if we are looking to implement any scale-rate based CGT in NZ, it should be done by a panel of experts who can discuss what the best tax rates are at each particular year. It might even be that we decide to go 0% after the 7th year, if that works out better for kiwi investors.

Also, it should be worth noting that any capital gains made on cashing out investment funds or kiwisaver should not be applicable to CGT as you are already paying a portfolio investment tax (PIR/PIE) on the returns made on those funds. No point in double taxing an investment that’s already been taxed.

On that same note, I think you shouldn’t be paying CGT on the sale of your first home/family home either – however this ruling will be subject to a clear and proper definition of what constitutes a ‘First/Family’ Home. Or the government could decide to do away with the legal hassle and make it a universal CGT on all properties.

In Conclusion

To wrap it all up – I will say that this country is likely to require some form of CGT to boost tax revenue. My only hope is that the government will implement a form of CGT that does not penalise individuals saving up for retirement.

I think many kiwis can get behind the idea of taxing property/share speculators through the nose but at the same time, we want to make sure that Mum and Dad’s (and our) investments are protected in the long run – hence why the time-based scale rate makes sense.

As always, share this article if it resonates with you and the more people we get reading it, the more debate we can have about this topic.

Discover more from The Comic Accountant

Subscribe to get the latest posts sent to your email.

Shivan

admin